A flooring adhesive market rarely turns on one headline. It shifts through lead times, resin costs, plant output, and jobsite demands. For 2026, the silane adhesive outlook for wood and resilient floors looks steadier than the last few years, but buyers still need to watch supply by formula, not just by brand.

That matters because low-odor, low-VOC products keep gaining ground. At the same time, glued engineered wood is holding up better, while vinyl and other hard surface categories still carry much of the volume.

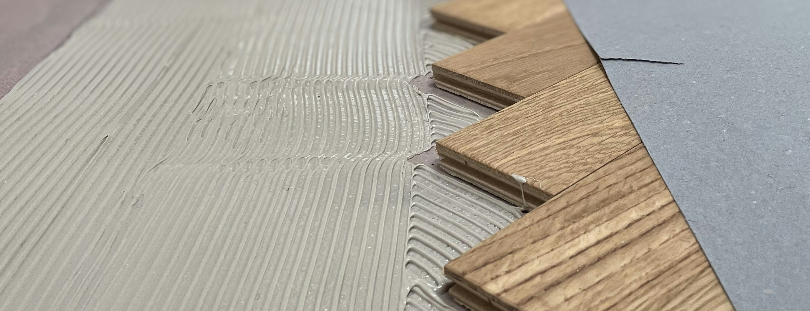

Demand is staying healthy in wood and vinyl

Silane adhesives keep winning share because they solve real field problems. Installers want strong grab, flexibility, and easier handling. Retailers want fewer odor complaints. Spec teams want products that fit tighter indoor air rules. Put those needs together, and silane stays in the conversation.

Recent flooring news on resilient demand points the same way. Resilient remains the volume driver, while wood has a better tone heading into 2026 than it had a year ago. That mix supports adhesive demand across both glued LVT and engineered wood.

At TISE 2026, suppliers put that trend on full display. Bona pushed its Quantum wood adhesives, with a message built around spread, strength, and lower emissions. Sika highlighted fast-set performance for LVT control. In other words, manufacturers aren’t backing away from silane, they’re building around it.

Demand alone doesn’t protect an installation, though. Moisture still decides a lot of the outcome, especially on slabs and mixed-use remodel jobs. That’s why teams planning glue-down LVT should review essential moisture tests for slabs under silane-based flooring adhesives. A premium adhesive can’t fix a wet substrate.

This also fits broader flooring trends. Buyers want fewer steps, cleaner chemistry, and systems that reduce callbacks.

Supply should improve, but it won’t feel loose everywhere

The good news is simple. Capacity looks better than it did when freight swings and raw material shocks hit harder. Several market trackers, including a recent flooring adhesive market forecast, expect steady category growth through the next several years. Silane-modified binders are also on a mid-single-digit growth path, which usually supports more plant investment.

Still, supply won’t feel wide open in every channel.

Silane products depend on modified polymers, additives, fillers, packaging, and dependable batch scheduling. If one input tightens, lead times can jump fast. The same resin families also serve construction sealants and other industrial uses, so flooring buyers don’t have the field to themselves.

Inside flooring manufacturing factories, producers are also tightening quality checks. Recent industry coverage around PFAS testing and material traceability shows how much more lab work now sits upstream. That raises confidence in finished goods, but it can slow approval of substitute inputs when a raw material changes.

The 2026 story is less about shortage, and more about formula-by-formula predictability.

Regional balance matters, too. New or expanded output in Asia helps global availability, yet North American buyers may still see tighter supply on niche SKUs, private-label programs, and slower-moving trowel grades. For wood and resilient floors, that means common products should be easier to source than specialty ones.

So the supply picture is better, just not lazy. Buyers who assume every adhesive is equally available may get caught flat-footed.

What buyers should watch at annual flooring shows and on the job

Current flooring industry news gives buyers two strong signals. First, demand for hard surface installs is still healthy enough to keep adhesive lines busy. Second, training and specification discipline are moving back to the center. NTCA education, Coverings sessions, and regional dealer events all point the same way: better prep, better documentation, fewer claims.

That helps explain why annual flooring shows still matter. Buyers use them to compare the newest flooring trends and products in person. They also use them to test the newest flooring products against real installer questions, like open time, ridging, cleanup, and bond control.

For distributors, retailers, and flooring companies, price still matters, but it shouldn’t be the first filter. A better buying conversation starts with four points:

- Lead time stability: Ask how supply changes if wood and LVT orders rise together.

- Approved substrates: Check moisture limits, patch compatibility, and slab conditions.

- Shelf life and storage: Fast-moving products age better than slow warehouse inventory.

- Change control: Ask what happens if a key raw material needs a reformulation.

If you’re selling glued wood over plywood or OSB, add wood subfloor MC checks for silane adhesive flooring success to that review. Many adhesive failures start below the plank, not inside the pail.

A steadier year, if you buy smart

Silane looks set for a better 2026 in both engineered wood and glued vinyl. Yet the strongest buyers won’t relax. They’ll track supplier depth, watch flooring news, and match every adhesive choice to the real jobsite. In short, predictability will beat bargain pricing in the year ahead.